Key Takeaways:

-

Say hello to financial freedom with our guide to the best 0% APR credit cards!

-

Whether you’re eyeing a shiny new laptop for work or unexpected car repairs have popped up out of nowhere — whatever your situation, a 0% APR credit card can be the superhero you need.

-

Join us as we take a closer look at zero percent cards, designed to help you fly high without the burden of interest!

Credit cards can be powerful tools for managing expenses and tackling existing debt. Imagine having the freedom to make purchases or transfer balances without worrying about interest charges for up to 21 months!

It’s a game-changer, especially if you’re stuck with high-interest debt. Having an introductory 0% APR credit card and using it wisely could save big!

Our selection of 8 top-notch cards with no interest for a specific period can help you maximize your savings.

What is 0% APR Credit Card?

A 0% APR credit card is a card that offers an introductory period during which no interest is charged on purchases and/or balance transfers.

This promotional period typically ranges from 12 to 21 months, depending on the credit card.

Cardholders can make new purchases or transfer existing balances without incurring interest during this period.

The 0% Intro APR cards are an exceptional tool for financial management, offering relief from the usual double-digit credit card interest payments.

What does 0% APR mean?

0% APR means that you will have no interest charged on certain transactions like qualifying purchases and balance transfers during a fixed period.

It allows cardholders to save money on interest payments and pay off debts more efficiently as long as they adhere to the terms and conditions of the credit card issuer.

With a 0% Annual Percentage Rate, you can carry a balance without accruing interest for a set time frame, typically ranging from 12 to 21 months.

However, late payments could nullify the card’s introductory 0% APR offer.

It’s important to note that minimum payments are still mandatory throughout the introductory APR period.

Plus, any remaining balance after this promotional period will accumulate interest at the regular APR.

How does 0% APR work?

A credit card with a 0% introductory APR allows you to make purchases and balance transfers without accruing interest for a set period.

While you still need to make monthly payments, any carried balance during this intro period won’t incur interest.

If you pay off your balance before the introductory period ends, you can avoid paying any interest altogether.

It’s essential to understand the terms and conditions of the offer before applying.

Best 0% APR Credit Cards

Unlock financial freedom with our guide to the top 0% APR credit cards. Whether you’re eyeing a big purchase or aiming to settle existing debt, these cards give you a break from interest charges.

Many zero-interest cards also come with enticing welcome bonuses and rewards, making them a smart choice for both short-term needs and long-term financial goals.

With introductory periods from 12 to 21 months, you can make the most of interest-free financing and potentially save hundreds of dollars. Let’s talk more about the best 0% APR credit card offers.

| Best Credit Cards with 0% APR | Introductory APR Period |

|---|---|

1. card_name |

intro_apr_rate,intro_apr_duration, then reg_apr,reg_apr_type |

2. card_name |

intro_apr_rate,intro_apr_duration, then reg_apr,reg_apr_type |

3. card_name |

0% Intro APR for the first 18 months on balance transfers, then reg_apr,reg_apr_type |

4. card_name |

intro_apr_rate,intro_apr_duration, then reg_apr,reg_apr_type |

0% Intro. APR for 15 months from account opening on purchases and balance transfers, then 20.49% – 29.24% variable |

|

6. card_name |

intro_apr_rate,intro_apr_duration, then reg_apr,reg_apr_type |

intro_apr_rate,intro_apr_duration on purchases and balance transfers, then reg_apr,reg_apr_type |

|

8. card_name |

intro_apr_rate,intro_apr_duration, then reg_apr,reg_apr_type |

Pros and Cons of 0% APR Credit Cards

Before applying for a credit card with a 0% APR intro offer, consider both its benefits and drawbacks carefully.

Pros

-

Savings on Interest: 0% APR credit cards allow you to save money on interest charges, regardless of the promotional period's duration. You can maximize your savings by paying off your balance before the Intro APR ends.

-

Reduced Monthly Payments: With no interest to worry about, your minimum monthly payment decreases. However, it's wise to pay more than the minimum to avoid accruing a substantial balance when the regular APR kicks in.

-

Faster Debt Payoff: Without any worry about interest charges, every dollar goes directly towards reducing your debt. It accelerates the debt repayment process, helping you become debt-free sooner.

-

Credit Score Improvement: Consistently making payments during the introductory APR period can boost your credit score, representing responsible credit management.

-

Potential Rewards: Many 0% APR credit cards offer amazing rewards, valuable perks, or welcome bonuses, providing additional benefits for cardholders beyond the interest-free period.

Cons

-

High-Interest Rates Post-Introductory Period: After the promotional 0% APR period ends, the interest rates can rise significantly. If the balance isn't paid off by then, the remaining balance will accrue interest at the card's standard rate, which could be quite high.

-

Fees and Charges: While these cards offer an interest-free period, there are often associated fees. Balance transfer fees, late payment fees, and annual fees can eat up any potential savings.

-

Impact on Credit Score: Opening a new credit card account, especially if it involves a balance transfer, can have a temporary negative impact on your credit score. Plus, missing payments or carrying high balances can further damage your credit score.

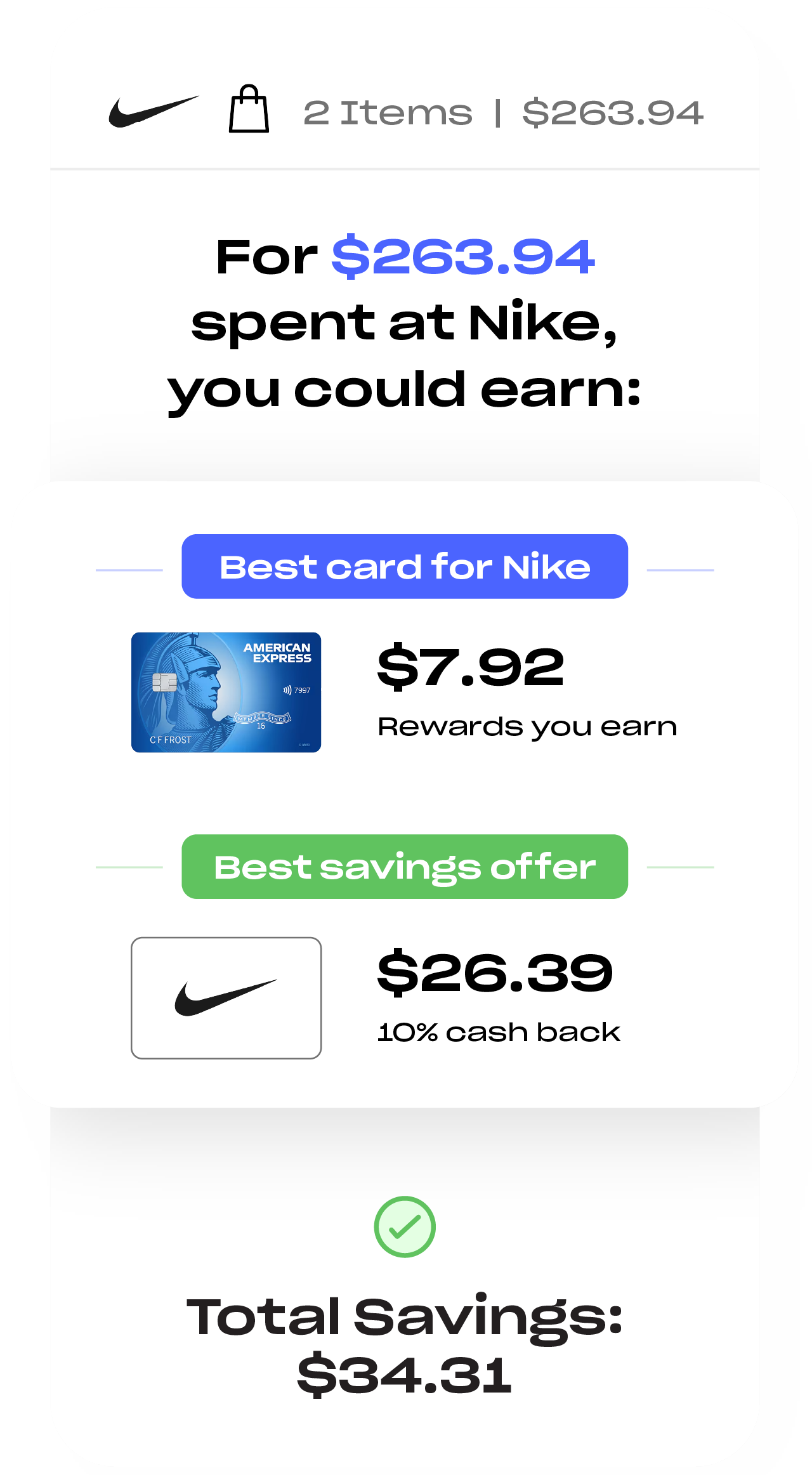

How much can you save with a zero-interest card?

A zero-interest card can lead to significant savings on interest payments. The amount you can save depends on the balance you carry and the length of the intro promotional period.

So, if you have a $5,000 balance on a credit card with an 18% APR and transfer it to a 0% APR card with a 12-month promotional period, you could potentially save about $900 in interest charges alone.

For example:- $5,000 X 0.18 = $900 annual interest

$900 / 12 = $75 monthly interest

$75 X 12 = $900 total interest saved

Using the best 0 APR credit card wisely, you can save a lot of money that would have otherwise gone for paying interest. Your savings will also depend on your ability to pay off the debt before the promotion expires and the potential fees.

Zero-interest credit cards can be beneficial in various situations. If you have multiple debts, transferring them to a 0% APR balance transfer card enables you to pay off or reduce the debt interest-free during the intro period.

The card provides an interest-free loan for significant upcoming expenses like buying furniture or car maintenance, provided you can clear the balance before the promotional period ends.

Choosing a zero percent card with generous welcome offers and rewards programs can further enhance savings, making these cards a financially savvy choice. Here are two examples of how much you can save with a zero-interest card:

-

card_name

With a intro_apr_rate,intro_apr_duration from account opening, this card provides significant relief from interest charges. After the introductory period, the APR ranges from reg_apr,reg_apr_type.

For a $6,000 purchase with a $300 monthly payment, you could save approximately $2,355 in interest.

-

card_name

Similar to the previous example, this card offers a intro_apr_rate,intro_apr_duration – with a variable APR between reg_apr,reg_apr_type after that.

If you make a $6,000 purchase and maintain a $300 monthly payment, you could save approximately $2,334 in interest charges.

How to choose a 0% APR card?

Selecting the right 0% APR credit card can be an excellent financial strategy to save on interest charges. These cards offer an introductory period during which no interest is charged on purchases or balance transfers.

Consider the following factors to ensure it aligns with your spending habits and financial goals:

-

Introductory Period Length

Introductory Period LengthThe time period of the 0% APR varies among cards, typically ranging from 12 to 21 months. Longer Intro APR periods provide more time to pay off balances without incurring interest charges.

Credit cards like the Wells Fargo Reflect Card and Citi Diamond Preferred Card offer the longest Introductory APR period of 21 months. (Terms Apply*) Some cards offer 0% APR on both purchases and balance transfers or one of them, each with its intro period.

-

Regular APR After Intro Period

Regular APR After Intro PeriodIt’s essential to check the regular APR that will apply once the introductory period ends. A lower regular APR can be beneficial if you expect to carry a balance after the promotional period.

While balance transfer credit cards can help you temporarily save on interest, you’re going to be stuck with the card’s regular APR for future purchases.

-

Balance Transfer Fees

Balance Transfer FeesSome 0-interest credit cards charge fees for transferring balances from other cards. Evaluate this balance transfer fee against potential interest savings to determine if a particular card is cost-effective for your needs.

Cardholders usually have to pay between 3% and 5% of the transferred amount, impacting their total repayment. Occasionally, issuers may waive this fee, so it’s worth considering when comparing cards.

-

Credit Score Requirements

Credit Score RequirementsQualifying for a 0% APR card often requires a good to excellent credit score. Make sure to assess your creditworthiness before applying, as multiple applications can temporarily lower your score.

-

Rewards and Benefits

Rewards and BenefitsWith the primary focus on the promotional APR offer, consider additional perks such as cashback rewards, travel benefits, or purchase protection that may enhance the card’s overall value.

Ask yourself if you’re interested in any other credit card benefits, such as a free FICO Score check, rewards on everyday spending, or cellphone insurance.

-

Annual Fees

Annual FeesDetermine if the 0% APR card charges an annual fee and weigh its cost against the benefits and potential savings from avoiding interest payments during the promotional period.

While the best 0% APR cards don’t charge an annual fee, others, especially those with lucrative rewards, may have one. Take into account the long-term cost, as some issuers waive the fee for the first year.

Who should get a 0% APR Credit Card?

You must have a good to excellent credit score to get the 0% APR card. The best zero percent credit cards can be highly beneficial in the following scenarios:

- Individuals who have existing high-interest credit card debt and want to consolidate debt to pay it off faster without accruing additional interest.

- 0% APR credit cards can be advantageous for those who are disciplined in managing their finances, making on-time payments, and having a plan to pay off the balance before the introductory period ends.

- Additionally, those looking to make large purchases and spread out payments over time without incurring interest can also benefit from a 0 APR card.

- If there is a sudden emergency like medical expenses and you wish to avoid high-interest charges.

How do you qualify for a 0% APR Offer?

To qualify for a credit card with a 0% APR offer, you generally need to have a good to excellent credit score, ranging from 670 or higher. Credit card issuers also consider your credit history, low debt-to-income ratio, and ability to make timely payments.

These increase your chances of qualifying for a 0% APR credit card. Additionally, meeting the income requirements set by the card issuer and having a stable financial background can also play a role in the approval of such promotional offers.

How to Compare 0% and Low Interest Cards?

Comparing 0% APR and low-interest credit cards involves understanding their distinct features and determining which aligns best with your financial needs and preferences.

Low-interest cards offer a consistently lower regular APR, making them suitable for those who often carry a balance.

They are often provided by credit unions and can be beneficial for ongoing balances.

On the other hand, zero APR cards provide a temporary opportunity to avoid interest charges entirely for a specified duration, typically 12 to 21 months.

They are useful for large purchases or balance transfers when you need time to pay off the amount without accruing interest.

However, their APR usually increases significantly after the introductory period ends.

While a 0% APR credit card can be advantageous for planned expenses, a low-interest card offers a stable APR that remains constant beyond any promotional period.

It is best suited for emergencies or situations where carrying a balance for a short period is unavoidable.

Understanding the differences between these two types of cards allows you to make an informed decision based on your financial position and goals.

| Feature | 0% APR Credit Cards | Low Interest Credit Cards |

|---|---|---|

Introductory APR Period |

Typically 12 to 21 months with 0% APR on purchases and/or balance transfers |

Generally no introductory 0% APR offer, but lower ongoing interest rates |

APR After Intro Period |

Variable APR applies after the promotional period ends |

The same lower ongoing APR rates apply |

Best Credit Card Options |

1. card_name 2. Citi® Diamond Preferred® Card 3. Wells Fargo Reflect® Card |

1. Gold Visa Card 2. Platinum Mastercard from First Tech Federal Credit Union 3. Choice Rewards World Mastercard |

If you’re uncertain whether to opt for a credit card with 0% APR or low interest, consider your financial needs and goals to determine the best option. These cards are particularly beneficial for paying down existing debt or financing new purchases without accruing interest for a specified period.

If you have a big purchase coming up and will need time to pay it off

Applying for a 0% APR credit card can be beneficial in this scenario, allowing you to make a large purchase and spread out the payments over an extended period without incurring interest charges.

For example, if you’re planning to buy a new laptop for $1,500 and can pay it off within the promotional 0% APR period, it can save you significant money compared to using a traditional credit card with high-interest rates.

It reduces your burden of large lump sum payments. However, it’s crucial to pay off the balance, or most of it, before the introductory offer expires to avoid accruing interest afterward.

If you find you’re consistently carrying a balance a from month to month

In this case, getting a zero APR card can provide temporary relief from accruing interest on your existing balance. You can easily transfer your balance to the new card and focus on paying off the principal amount without additional interest charges.

It’s vital to have a solid repayment plan to clear the debt before the promotional period ends, as high-interest rates may apply after that. But if you find yourself frequently carrying a balance from month to month, a low-interest credit card could be a more suitable option for you.

If you want to transfer a balance to pay it down at a lower cost

A zero-interest credit card can be useful for balance transfers, especially if you’re looking to consolidate debt from high-interest cards to one with no interest for an introductory period.

For instance, transferring a $5,000 balance from a card with an 18% APR to a 0% APR card can save you hundreds of dollars in interest fees during the promotional period. Review and understand any transfer fees applicable and the length of the introductory APR period before making the decision.

Look for cards with low or no balance transfer fees to minimize your costs. Be mindful of the time frame within which you need to request the transfer, as some cards have specific requirements.

After deciding the type of card you want, compare cards based on the following factors

-

Introductory APR Period

It is the most common feature for comparison among the several credit cards. Introductory APR periods often extend to a year or more upon account opening.

Along with an interest-free period, these cards offer various reward options, making them ideal for big purchases. Remember that missing a payment could result in the cancellation of the 0% rate, leading to high-interest charges.

Some cards may offer extended 0% periods for balance transfers but shorter or no intro periods for purchases.

When choosing the lowest APR card, the length of the introductory APR period is crucial – longer durations provide more time to pay off balances without incurring interest.

-

Ongoing APR

The ongoing APR, also known as the regular APR, is an important factor to consider while choosing a credit card, especially if you anticipate carrying a balance beyond the intro 0% APR period.

Cards with zero percent interest often come with higher regular APRs compared to low-interest cards. This rate determines the interest charged on any remaining balance once the introductory period expires.

Therefore, it’s essential to carefully evaluate the regular APR to calculate the potential cost of carrying a balance in the long term and select a card that aligns with your financial needs and habits.

-

Balance Transfer Fee

It is a crucial aspect to consider when moving debt from one credit card to another. Typically ranging from 3% to 5% of the transferred amount, the balance transfer fee can add up quickly, costing $30 to $50 for every $1,000 transferred.

If you’re transferring a balance to take advantage of a promotional 0% introductory rate, the fee may be worthwhile if it outweighs the interest saved.

Ensure to calculate your savings against the fee and explore card options with no balance transfer fees for cost-effectiveness.

-

Required Credit Profile

Required Credit ProfileTo be eligible for a 0% APR credit card, you must have a good credit profile, typically requiring a credit score of 690 or higher. Some cards may even demand excellent credit – often 720 or above.

Having a good credit profile not only increases approval chances but also enhances your access to favorable terms and conditions.

Regularly monitor your credit score and try to boost your credit score for better card options and financial opportunities.

-

Penalty Policies

Penalty PoliciesTimely bill payment is important to avoid unnecessary penalties. Missing a payment typically incurs a hefty fee, often around $40, and delays of 30 days or more can severely impact your credit score.

Moreover, late payments can trigger a penalty APR, skyrocketing your interest rate up to 30% in some instances. Ensure to review your card’s penalty policies.

-

Annual Fee

Annual fees can drain your savings, especially with low-interest or 0% APR credit cards, where saving money is paramount! While most cards have no annual fee, some rewards cards with 0% interest periods may charge one.

Make sure the rewards earnings, and benefits outweigh the cost of the card to maximize your overall savings and financial well-being.

-

Free Credit Score

Free Credit ScoreAccess to a free credit score is a valuable perk offered by various credit card issuers, providing cardholders with insights into their financial health.

It is very helpful to keep track of your progress and identify areas for improvement, especially when managing debt.

By knowing your credit score, you can take proactive steps to maintain or increase it for greater financial stability and unlock better credit offers in the future.

-

Rewards and Bonus Offers

They can significantly enhance the value of a 0% APR credit card, providing additional benefits beyond interest savings.

Like cash-back cards with a 0% introductory period allow you to earn rewards on purchases, effectively reducing the overall cost.

For instance, spending $3,000 on a card offering 1.5% cash back and a $200 welcome bonus for qualifying purchases can result in $245 cash back, effectively reducing the purchase cost to $2,755.

Beyond rewards and bonus offers, cardholders can enjoy perks like purchase protection and travel benefits, which add further value while prioritizing debt repayment.

How to make the most of a 0% APR offer?

Utilizing 0 APR credit cards effectively can be a smart financial move. You can maximize the benefits of your card’s 0% APR offer in the following ways:

-

Apply at the right time

Timing is very crucial when applying for a card with 0% APR. Applying during promotional periods or when you have planned expenses can help you make the most of the interest-free period.

This helps you to strategically maximize the perks and ensures more time to save on potential interest charges.

-

Understand the offer entirely

Before committing to a zero-percent APR offer, ensure you understand all terms and conditions to avoid any surprises. Pay attention to any potential fees, balance transfer limits, and the duration of the promotional period.

You can also prevent these by setting up automatic payments, transferring balances promptly, and meticulously reviewing terms.

-

Calculate your monthly payments

To fully benefit from a 0% APR offer, plan your monthly payments to clear your balance before the promotional period ends. This will help you avoid accruing interest once the offer expires.

Always prioritize paying above the minimum, and steer clear of accumulating debt. Utilize tools like Uthrive’s payment calculator for precise estimations.

-

Don’t close the card after the intro APR period ends

Keeping the card open even after the introductory APR period is over can be beneficial for your credit score. Immediately closing it may impact your credit utilization ratio, negatively affecting your credit score.

Try to maintain your card for a positive credit history and boost your creditworthiness.

FAQs

How does credit card interest work?

Credit card interest works by charging you a percentage of the outstanding balance on your credit card that you haven’t paid off. It is known as the Annual Percentage Rate (APR).

The APR can vary based on factors like your credit score and the type of transaction. If you carry a balance on your card, you will be charged interest on that balance each month until it is paid off.

How can I get 0% APR on an existing credit card?

To get 0% APR on an existing credit card, look for promotional introductory offers from your credit card issuer. Sometimes lenders might offer 0% APR to existing credit card holders if they have a good credit history.

With this, you get a specified period during which you won’t be charged any interest on new purchases and/or balance transfers.

What determines the APR on a credit card?

The APR on a credit card is determined by several factors, including the prime rate set by the Federal Reserve, the issuer’s profit margin, and your creditworthiness.

Your credit score plays a significant role in determining the APR of the card – generally, the higher your credit score, the lower your APR may be.

What is the best credit card with no interest?

The best credit card with no interest would depend on your financial needs and spending habits.

Some popular options offering an introductory 0% APR period on purchases or balance transfers include the card_name and Citi Simplicity® Card.

What credit score is required for a 0 percent APR card?

You typically need a good to excellent credit score for a zero percent APR credit card, which generally ranges from 670 to 850.

What is the longest 0% period I can get on a credit card?

The longest 0% interest period you can get on a credit card is 21 months with no interest charged on purchases or balance transfers during that time frame. This introductory period varies depending on promotional offers from different issuers.

What is a purchase interest charge?

A purchase interest charge is the fee applied when you carry a balance from one month to another on purchases made using your credit card.

This charge accrues daily based on your average daily balance and your card’s APR until you pay off the outstanding amount in full.

How much will my credit card payment be with 0% APR?

The monthly payment on a credit card with 0% APR depends on the total balance you owe and the repayment term. To calculate the payment, divide the total balance by the number of months in the promotional period.

For example, a $1,000 balance over 12 months would require payments of approximately $83.33 per month.

What happens when the 0% APR offer ends?

When the 0% APR offer ends, the credit card issuer will start charging interest on any of your remaining balances at a regular APR. It is important to pay off the balance before the promotional period ends to avoid accruing high-interest charges.

What are the longest 0% APR credit card offers?

Popular credit cards like the Wells Fargo Reflect® Card, Citi Simplicity® Card, and Citi® Diamond Preferred® Card offer the longest 0% APR period with no interest on purchases and balance transfers for the first 21 months.

Is deferred interest the same as a 0% APR credit card?

Deferred interest and 0% APR are not the same. With deferred interest, the interest accrued during a period is not charged if the balance is paid in full by the end of that period.

On the other hand, a 0% APR credit card offers no interest on purchases or balance transfers for a specified promotional period, regardless of whether the balance is paid in full by the end of the period or not.

What is the difference between interest rate and APR?

Interest rate refers to the cost of borrowing money you pay to a lender while Annual Percentage Rate (APR) is the interest rate and other fees and charges associated with borrowing – the total cost of borrowing over one year. Both of these are expressed as a percentage.

How can I qualify for a low interest credit card?

To qualify for a low-interest credit card, you typically need a good to excellent credit score (generally above 670). Lenders also consider other factors like your history of responsible credit use, a stable income, and a low debt-to-income ratio.

Which is better: low APR or cash back?

If you often carry a balance, a low APR card can save you money on interest charges. On the other hand, if you pay off your balances in full each month and want rewards, cashback cards are an excellent option to earn on your expenses.

Ultimately, the choice between low APR and cash back depends on your financial goals. Consider your spending habits and preferences when deciding between these options.

![Guide to Houston Intercontinental Airport Lounges: Top Things to Know [2025]](https://www.uthrive.club/wp-content/uploads/2024/11/Guide-to-Houston-Intercontinental-Airport-Lounges-Top-Things-To-Know-2024-1024x600.jpg)

![Guide to Seattle Airport Lounges: Top Things to Know [2025]](https://www.uthrive.club/wp-content/uploads/2024/11/Guide-to-Seattle-Airport-Lounges-Top-Things-To-Know-2024-1024x599.jpg)

![Guide to LaGuardia Airport Lounges: Top Things to Know [2025]](https://www.uthrive.club/wp-content/uploads/2024/10/Guide-to-Laguardia-Airport-Lounges-Top-Things-To-Know-2024-1024x600.jpg)

![Guide to SFO Airport Lounges – Top Things to Know [2025]](https://www.uthrive.club/wp-content/uploads/2024/10/Guide-to-SFO-Airport-Lounges-Top-Things-To-Know-2024-1024x599.jpg)

![Guide to Boston Airport Lounges: Top Things to Know [2025]](https://www.uthrive.club/wp-content/uploads/2024/10/Guide-to-Bostan-Airport-Lounges-Top-Things-To-Know-2024-1024x600.jpg)